While lamb has seen a strong market this season, cull dairy cows have clogged the beef trade. Reece Brick reports.

We’re coming up to the half-way point of the 2018-19 red meat season and it’s fair to say it’s been a solid few months, though it’s not been all sunshine and rainbows for everyone. Instead there seems to be a rebalancing of sorts happening in a few different areas.

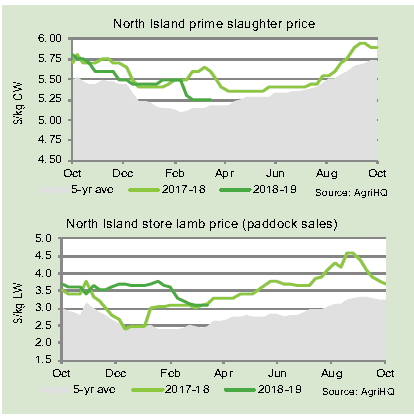

Lamb has easily been the strongest market. Nerves about a collapse like we saw in 2011-12 have faded into oblivion. Ongoing demand from China has essentially cancelled any negativity out of the United Kingdom. Instead schedules have only just edged below last year’s already very high levels but look to be near their bottom, assuming nothing out of left field shakes things up.

Store lambs have looked like a bargain versus what was being paid before Christmas. However, in the grand scheme of things they’re still putting a good amount of cash in vendors’ pockets.

From early-February to mid-March store lambs still made 15c/kg more than a year ago in the yards, averaging out at $3.40/kg at 32kg in Feilding and Stortford Lodge and $3.45/kg at 30kg in Canterbury Park and Temuka.

On the beef side of the equation it’s all come back down to earth.

An early influx of cull dairy cows has clo gged the system, a situation that’s likely to be unchanged until Gypsy Day in early June.

gged the system, a situation that’s likely to be unchanged until Gypsy Day in early June.

Combine that with a middling export market and kill sheets make for mediocre reading.

Schedules are down 35-45c/kg on last year for steers and back 45-60c/kg on bulls.

Luckily, finishers have found some relief when restocking at the early beef weaner fairs. On average steers and heifers have trailed last year’s prices by $150-$200 through the North Island. For example, traditional and exotic steers averaged $3.65/kg or $920 at the first Stortford Lodge fair, down from $4.25/kg or $1060, and heifers were $3.15/kg or $710, down from $3.70/kg or $850. South Island fairs were yet to begin at the time of writing.

Venison has smacked its ceiling with a thud and is falling back to territory that is more sustainable longer-term. Schedules have fallen weekly for five-months straight but are still comfortably at their second-highest ever for this point in the year, which just goes to show how high they managed to climb in the first place.

Exporters appear confident that the market will realign in the next few months before it really begins to hurt deer farmers’ back pockets.