The beef crystal ball

The fundamentals of global supply and demand are underpinning tight supply and strong demand to continue, says the latest RaboResearch report into the global beef trade signals. Words Sarah Perriam-Lampp.

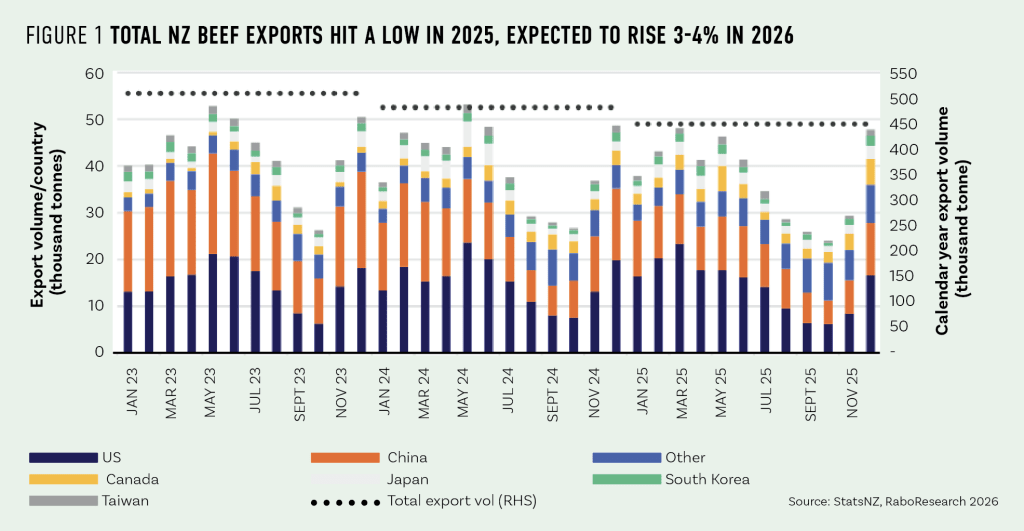

New Zealand beef farmers head into 2026 farming in a world that is volatile geopolitically, but RaboResearch Animal Proteins Analyst, Jen Corkran, suggests that the fundamentals of trade are still strong.

The latest 2026 Q1 RaboResearch Global Beef Quarterly points to an extended period of tight global supply and robust demand – especially for the kind of product New Zealand does best: high-quality trim and manufacturing beef.

According to Jen, the big picture is that there simply isn’t enough beef in the world for the level of demand, particularly in the northern hemisphere.

“Fundamentally, there is not enough beef around the world for the amount that’s potentially wanting to be eaten, which has created the strong prices.”

For New Zealand producers, that tightness is expected to underpin continued strength in export pricing over at least the next two to three years, even as geopolitics, trade policy and shifting trade flows add layers of uncertainty.

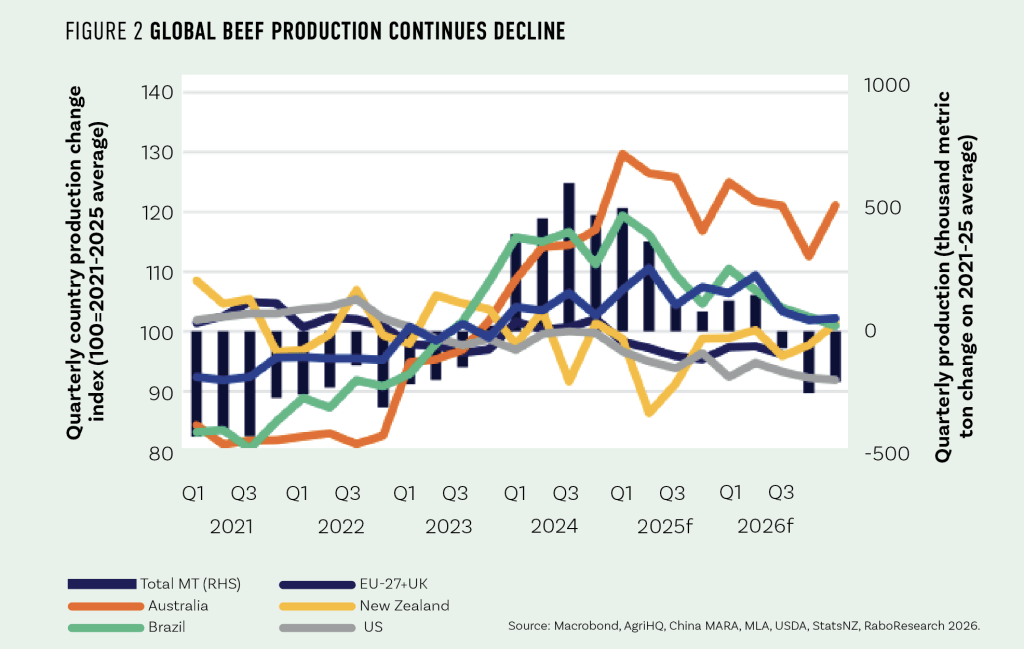

Global supply still below the five-year average

The latest report looks through 2026 and compares global beef production back to the period from 2021 to 2025. The signal is consistent in that total global beef supply this calendar year is expected to sit below the five-year average.

Jen notes that global production is forecast to be roughly 1-2% down on the 2021-2025 average. That might sound modest, she says, but in a tight market

it’s enough to keep a firm floor under prices, particularly when demand remains resilient across key importing regions. She says for New Zealand, that environment plays directly into our strengths.

“Into the US, our exports are weighted toward trim and manufacturing beef, feeding into burger patties.”

The US are crying out for import volume of this lean trim, this is what is in high demand. As a result, average export values remain elevated. While prices can’t climb forever, she suggests we are still in an environment of historically high returns for manufacturing beef, particularly into the United States.

How fast will the US cow herd re-build?

The US remains the central story in global beef. After several years of aggressive cow culling, driven by drought and high feed costs, the US beef cow herd is at a 75-year low.

Even though this has been talked about repeatedly, Jen says producers may still underestimate how long and how tight this phase could be.

The US is now in the early stages of trying to rebuild its beef cow herd. In addition, while the US has some additional supply coming from beef-on-dairy cross animals, Jen says, that doesn’t fully solve the shortage of lean trim.

“To do that, producers must stop culling cows, which in turn starves the system of cull-cow trim which New Zealand services. At the same time, burger demand is holding up well.”

For New Zealand and Australia, this shortage has translated into exceptional demand and pricing for manufacturing beef.

“What we’re producing, compared to some of the other markets, is the exact product that they want, and it is a consistent, quality product. It’s consistently the right specifications. So we’re in a good spot.”

What about Brazil?

Brazil is expected to increase its presence in the US market in the second half of the year, redirecting some product away from China following the announcement of China’s new import quota. But Jen is clear that New Zealand’s role is still differentiated.

“We’re in a real specific kind of sweet spot around premium. It’s what some people would call a commodity beef product, but actually it’s a consistent, amazing product that’s grass-fed.”

She reiterates that even with more Brazilian beef entering the US, New Zealand manufacturing is currently sitting at such a high that some easing would still leave returns well above historical averages.

“We’ve been at 40-50% above that five-year average price for 90CL and 95CL beef going into the United States. Even if we come off that huge high, we’re still elevated.”

The upshot for New Zealand producers: steady to firm pricing into the US is still the central scenario, assuming no major global demand shock.

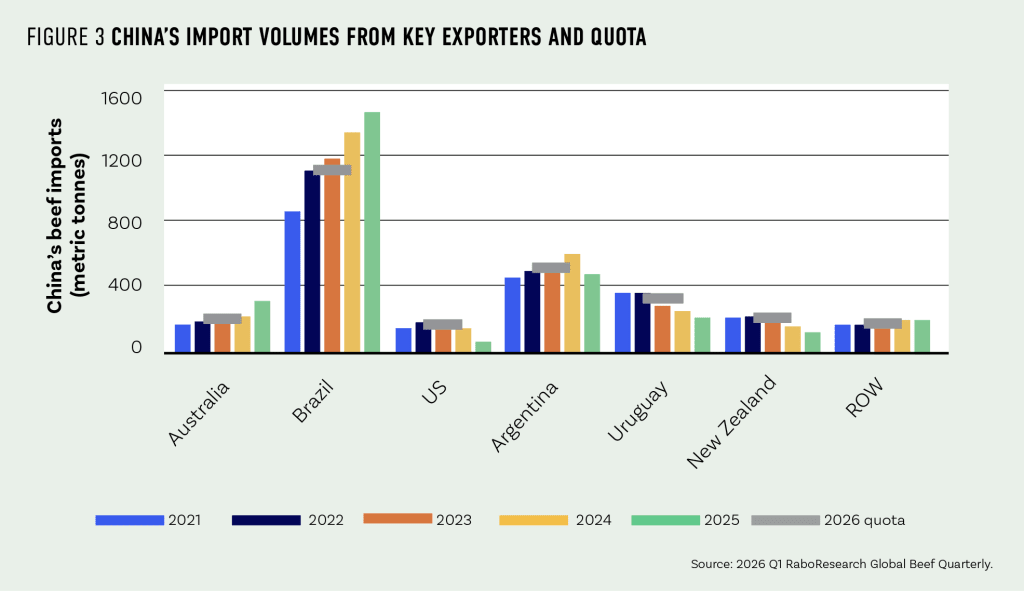

China’s new beef import quotas

If the US is the primary demand engine, China’s new beef import quota system is the big structural shift reshaping trade flows.

After years of growing beef imports – much of it from Brazil – Chinese cattle farmers have pushed back against increasing competition from cheaper imported product. In response, Beijing has implemented a “safeguard” import limit, capping volumes for major exporters including Brazil, Australia, New Zealand, Uruguay, Argentina and the US.

Jen explains the quota is broadly based on the average volume imported over a multi-year period, and if a country exceeds its limit, any additional product faces a punitive 55% tariff – effectively a trade stopper.

“If you go over your quota limit, you get a 55% tariff. It is unlikely importers in China will pay that. They’ll just say, ‘No, that’s it.’ We believe it’s a trade stopper.”

For New Zealand, the picture is surprisingly positive, she says. Because our exports to China have been well below historic highs in the last couple of years, we have significant headroom under our quota.

“We could send another 40% of volume compared to 2025 and we still would only just hit the quota that we’re given.”

Brazil and Australia are in a very different position. In recent years, Brazil has supplied ~50% of China’s imported beef. Australia also shipped more than it’s quota in 2025. So both countries will need to find new homes for substantial volumes.

For Australia, the shortfall is around 100,000 tonnes – close to the total volume New Zealand sent to China last year.

“That redirection is likely to create some short-term competition in other markets. But for New Zealand, the rebalancing may open up opportunities both in China and beyond.”

However, she says, China’s domestic beef production is expected to decline by around 4.4% YOY. So she believes China may pay more for certain cuts, including briskets and other forequarter items, as supply tightens. It will be the shift and movement in trade flows and price points paid that will be a what to watch in 2026. And there may also be spillover benefits for sheepmeat pricing in the second half of the year if Chinese protein buyers are short of beef.

“I also think we might see China perhaps paying a little bit more for red meat protein in the second half of this year. We’ve already seen an increase in local beef prices in China in January.”

Geopolitics impact on farm costs

On the other side of the ledger, attractive export prices may be the essential buffer farmers need as input costs on farm may be impacted by war in the Middle East. The report itself was finalised before the latest escalation in the Middle East, but Jen notes that recent events are likely to add further pressure to fuel and fertiliser prices, particularly urea.

“Up to 45% of global Urea supply comes out of that region.” Those rising inputs threaten to erode margins, even against better schedules. Jen’s advice is not necessarily to dwell on every twist in geopolitics, but to understand the underlying fundamentals: if beef prices hold firm while input costs lift, some of the sting is at least partially offset.

“If we’re getting paid better for our products, it helps those margins that would otherwise be squeezed even more.”

Jen believes we are heading toward a natural ceiling in beef prices as consumers eventually push back, particularly in markets where beef has become very expensive at retail. But for now, there is still room for New Zealand’s key markets to pay for the product they need.

For farmers making decisions on stocking rates, capital investments or debt, the message from Jen is to balance earnest confidence in the fundamentals with caution around costs and volatility. The world may be uncertain, but for the next couple of years at least, global beef looks set to remain one of the more resilient stories in agriculture.